Ready to finance a used car? This blog will empower you to break down the world of used car loan rates and financing, showing you exactly what lenders charge for used car loan rates and financing, how the borrower credit score plays an important role, and the steps you can take to drive away with a loan that fits your budget completely.

What are Used Car Loan Rates and Financing?

Used car loan rates and financing are the processes of borrowing money from lenders to purchase a pre-owned vehicle. The interest rate charged by the lender, typically a monthly percentage, is heavily influenced by your credit score. A good used car loan financing without a credit check score can secure you a lower rate on your borrowings. Various lenders, such as banks and finance companies, offer different interest rates on borrowing.

The financing process of borrowing starts with deciding your budget for the used car you are interested in and then reviewing your credit score. You can then explore loan options from various lenders in the marketplace. Once you find a car, you can apply for a loan, and the lender will go through your application. If you are approved, you will sign loan papers, and the money goes to the seller. You will then make monthly installments. Rest assured, you must ensure that you compare rates and fees before you commit to the lender.

What are Current Auto Loan Rates and Financing?

As of March 24, 2025, current used car loan rates and financing range from around 6.40% to 9.59% depending on credit score, while used cars range from 7.41% to 14.46%. Following is a list of some Bank of America used car loan rates

|

Lender |

Best For |

Starting APR’s |

Loan Term |

Loan Amount |

|

Southeast Financial Credit Union |

Short-term loans with cheap rates |

3.50% |

12-84 months |

Up to $100,000 |

|

Navy Federal Credit Union |

Those with military connections |

4.09% |

12-96 months |

Starting at $250 |

|

PenFed Credit Union |

Car shopping and comparing sticker prices |

4.09% |

36-84% |

Up to $150,000 |

|

Autopay |

Bad credit auto loans |

4.85% |

24-96 months |

$2,500-$100,000 |

|

Bank of America |

Those who prefer large banks |

5.54% |

48-72 months |

Starting at $7,500 |

|

DCU |

Used car loan |

5.74% |

Up to 84 months |

Up to 130% of the car’s value |

|

Carmax |

An online experience |

5.75% |

24 to 72 months |

$500 – $100,000 |

|

Capital One |

Best car loan overall |

5.89% |

24-84 months |

Starting at $4,000 |

|

LightStream |

Quick car loans |

6.94% |

24-84 months |

$5,000-$100,000 |

|

PNC |

Private-party auto loans |

8.44% |

12-84 months |

$5,000- $100,000 |

How does an Auto Loan Work?

You use an auto loan to buy a car without paying the full amount to the dealership. You borrow money from some lenders or financing companies and then pay it back with monthly payments, including interest and fees. A down payment might not be mandatory, but it’s often a good idea as it lowers your borrowing amount and overall costs.

While making payments, you’re the registered owner of the used car, but the loan company or lender from where you took the loan is technically owned of the car. With a secured loan, your car serves as collateral. If you miss too many payments, the lienholder can repossess your car.

Once you’ve paid the loan in full, the lender will release the car’s title to you. Only then does the car officially become your property. So, you borrow, you repay with extra costs, and ownership transfers after full payment, concluding the financial aspect of the used car sale process.

5 Types of Used Car Loans in the Automotive Industry

When you look for the best used car loan rates and financing, you will see several loan types, such as used auto loans, online lenders, P2P lending, and many more.

1. Used Auto Loan

Used auto loans typically carry higher rates than new car loans. Additionally, some lenders have specific rules about the vehicles they will finance. For instance, some may not finance a vehicle that is 10 years old or older.

2. Bank Loans

Banks and credit unions are probably the places most people think of first. You can just go into your neighborhood bank or credit union and ask to apply for a used car loan.

3. Online Lenders

The Internet has opened a whole new world of lending money to borrowers. Numerous online platforms in the used car marketplace specialize in auto loans, including those looking for used cars.

4. Peer-to-Peer Lending

These platforms connect borrowers directly with individual investors. You can find that the rates can be decent, but it might be a smaller market for used car loan financing rates

5. Private-party Auto Loan

You can finance a car from a person instead of a dealership. These loans can be harder to find, but you may have luck searching with banks and credit unions.

Top 5 Benefits of Auto Loans in 2025

Though there are some drawbacks, securing the best used car loan rates and financing loans also comes with perks that other ways of getting a car do not. You’ll spread out the expense, may be able to afford a better car, and could have a boost to your credit with consistent on-time payments.

1. Pay Less Upfront, Borrow Less Cash

Used cars have a much lower price tag than new cars, meaning you won’t need to borrow as much money to buy a used car from a dealership lot.

2. Enjoy Easier Monthly Payments

Since you’re not borrowing a huge money from the lender, your monthly loan payments can be quite a bit lower, giving your wallet some breathing room.

3. Skip the Big Value Drop

New cars lose a ton of their worth in the first couple of years. When you buy used, someone else already ate that depreciation cost.

4. More Car for Your Cash

Buying a used car means your money buys more. You can often get a better-equipped model with more cool features than if you bought a new used car for the same amount of money.

5. Knock Out Your Loan Faster

Because the loan amount is typically smaller, you’ll often have the chance to pay off your used car loan financing quicker, which means less interest paid over time.

How Your Credit Score Impacts Your Used Car Loan Rates and Financing: A Detailed Explanation

Your credit score plays a major role in getting the best used car loan rates and financing. It’s a big deal for the interest rate you’ll end up paying. People with higher credit scores have a history of paying their bills on time. Lenders know this, so they see these borrowers as less risky. Because of that, they’ll offer people with good credit lower interest rates to get their business. It’s like a reward for being responsible with your credits.

Additionally, dealerships and auto loan providers are leveraging automotive SEO services to attract customers by optimizing their online presence, helping consumers find the best deals on used cars and loans.

Now, by looking at some numbers from the third quarter of 2024. You can see the average Annual Percentage Rate (APR) for used cars, and it jumps depending on the credit score.

|

Credit Score |

Average used car APR |

|

Super prime (781-850) |

7.41% |

|

Prime (661-780) |

9.63% |

|

Nonprime (601-660) |

14.07% |

|

Subprime (501-600) |

18.95% |

|

Deep subprime (300-500) |

21.55% |

Say a borrower wants to borrow $25,000 for a used car and plans to pay it back over 60 months.

Example

If the persona has a super prime credit score of 781 to 850, he is looking at an average interest rate of 7.41%. Over those five years, he will end up paying about $4,993 in total interest. Now, if your credit score falls into the deep subprime range, that’s 300 to 500, the average used car auto loan rate jumps way up to 21.55%. On that same $25,000 loan over 60 months, you’d be paying a staggering $16,045 in total interest!

As your credit score plays a major role in the APR you will get for your auto loan, it can make a huge difference in how much you ultimately pay for your used car. A good credit score can save people from losing tons of money. For dealerships, understanding customer credit profiles is also important for managing risk and optimizing sales, and this can sometimes be integrated with used car inventory management software to offer tailored financing options.

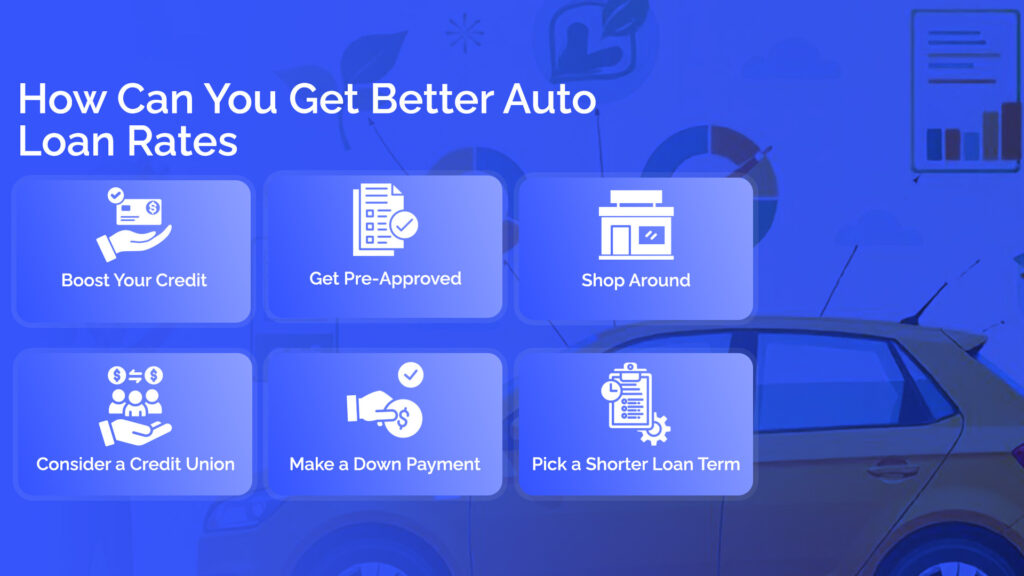

How Can You Get Better Auto Loan Rates?

If you have a high credit score above 750, make a higher down payment, choose a shorter repayment tenure, and have a steady source of income, you can negotiate with the lenders to offer you a lower interest rate on used car auto loan rates.

1. Boost Your Credit

Borrowers should actively work to improve their credit scores. A borrower with a higher credit score shows responsibility and unlocks lower interest rates on the auto loan.

2. Get Pre-Approved

Borrowers should get pre-approval for their car loan before visiting the used car dealerships. This shows the borrowing power and provides leverage for negotiating a better rate.

3. Shop Around

Borrowers should always compare the loan offerings from various lenders like banks, credit unions, and online platforms to find the most favorable interest rates and terms.

4. Consider a Credit Union

Always explore membership options at credit unions or other platforms. This is because they frequently offer the lowest used car loan rates to their members.

5. Make a Down Payment

Borrowers should voluntarily put money down at the time of car purchase. This reduces the lender’s risk and helps you secure a lower interest rate on the loan.

6. Pick a Shorter Loan Term

Choose a shorter repayment period if your budget allows you. Longer loan terms often come with higher overall interest rates, which automatically makes you pay tons of money.

Top 6 Ways to Compare Auto Loan Rates

Getting a great used car loan rates and financing means comparing rates wisely. This guide shows you key factors like APR, loan terms, fees, and lender reputation to help you make a smart choice and save money. For those in the used car business setup, understanding these comparison points is crucial for guiding customers.

1. APR (Annual Percentage Rate):

APR measures the total yearly cost of your loan, including interest and fees. A lower APR makes your used car loan rates and financing cheaper.

2. Loan Amount

Unless you are buying a luxury car, you probably won’t need to worry about maximum loan amounts. But if you want to finance a cheaper used car, not all lenders can accommodate. Most auto loan amounts start at several thousand dollars.

3. Financing Term

Your financing term is the length of time you have to pay off your loan. Terms between 12 and 84 months are the most common. The longer your term, the lower your monthly payment usually is. On the other hand, a long-term loan could also mean more interest over the life of the loan.

4. Fees

Buying a car can come with mandatory fees, like taxes, titling, and registration. Some dealer fees are optional, like those associated with protection packages and extended warranties. Always ask for the out-the-door price, and don’t be afraid to turn down options that you aren’t interested in. You can analyse the price by looking at used car price trends.

5. Unique Features

Outside of cheap rates, think about what is important to you in an auto loan. Perhaps you prefer to pay by using a mobile app, or maybe you need some help with car shopping and are interested in a car-buying service. Seek out lenders that offer those perks.

6. Lender Reputation

Unless you refinance your auto loan, you’ll be stuck with your auto loan lender until you pay off your car. Avoid getting stuck with a bad company by reading customer reviews. LendingTree lender reviews offer a good place to start. You should also check for official complaints on the Consumer Financial Protection Bureau (CFPB) customer complaint database.

How to Choose the Best Picks for Your Auto Loan Rates

The following are some key factors you should keep in mind when choosing the best pick for your used car loan rates and financing.

1. Easy Access & Clear Process.

The borrower should choose lenders who can simplify the borrowing process. Look for easy qualification requirements and transparent, step-by-step processes for pre-approval, application, and receiving your funds quickly.

2. Low Rates & Flexible Options.

Seek out lenders with attractive starting interest rates that stay consistent. Prioritize those who keep fees to a minimum and provide a range of choices for how much you can borrow, how long you have to pay it back, and any potential savings on the overall loan cost.

3. Good Service & Easy Repayment.

Pick lenders known for treating customers well and having a solid track record. Ensure they offer helpful support when you need it and provide convenient ways to manage your payments, such as through easy-to-use mobile apps. Any extra benefits they offer are a bonus.

Conclusion

Getting a used car loan rates and financing means you borrow money to buy the car and pay it back every month with extra interest. Your credit score is key for getting a good interest rate. Shop around at banks, credit unions, and online. Compare the total cost (APR), loan length, and fees. A good loan helps you drive your car without emptying your wallet upfront.